The Question Your Lender No Longer Answers for You

Your lender required full coverage when you financed the car. Now the title is yours, your carrier says you can save money by dropping collision and comprehensive, and you're standing at a decision point most insurance advice skips: can you replace this car out of pocket if you total it next week? That question has a dollar answer, and it lives in your checking account, not in generic coverage guides.

Edison drivers with paid-off vehicles face the same structural choice. New Jersey still requires liability, personal injury protection, and uninsured motorist coverage whether you own the car outright or not. Collision and comprehensive become optional the day the lien releases. The decision framework isn't complicated, but it requires knowing what your car is actually worth and what you can actually afford to lose.

Compare rates from carriers that specialize in senior drivers

Mature driver discounts, low-mileage rates, and coverage reviews — see what you're actually eligible for.

Get Your Free QuoteNJ Bodily Injury Minimum Per Person

$15,000

New Jersey's minimum liability limits are $15,000 per person, $30,000 per accident, and $5,000 property damage. That floor protects others in an accident you cause, not your own vehicle—collision and comprehensive are the only coverages that pay to fix or replace your car.

N.J.S.A. 39:6B-1

What Full Coverage Actually Covers Once the Car Is Yours

Liability, PIP, and uninsured motorist coverage are mandatory in New Jersey and remain mandatory after you pay off the car. Those coverages pay for injuries and damage you cause to others, your own medical bills under PIP, and protection when an uninsured driver hits you. None of them pay to repair or replace your own vehicle.

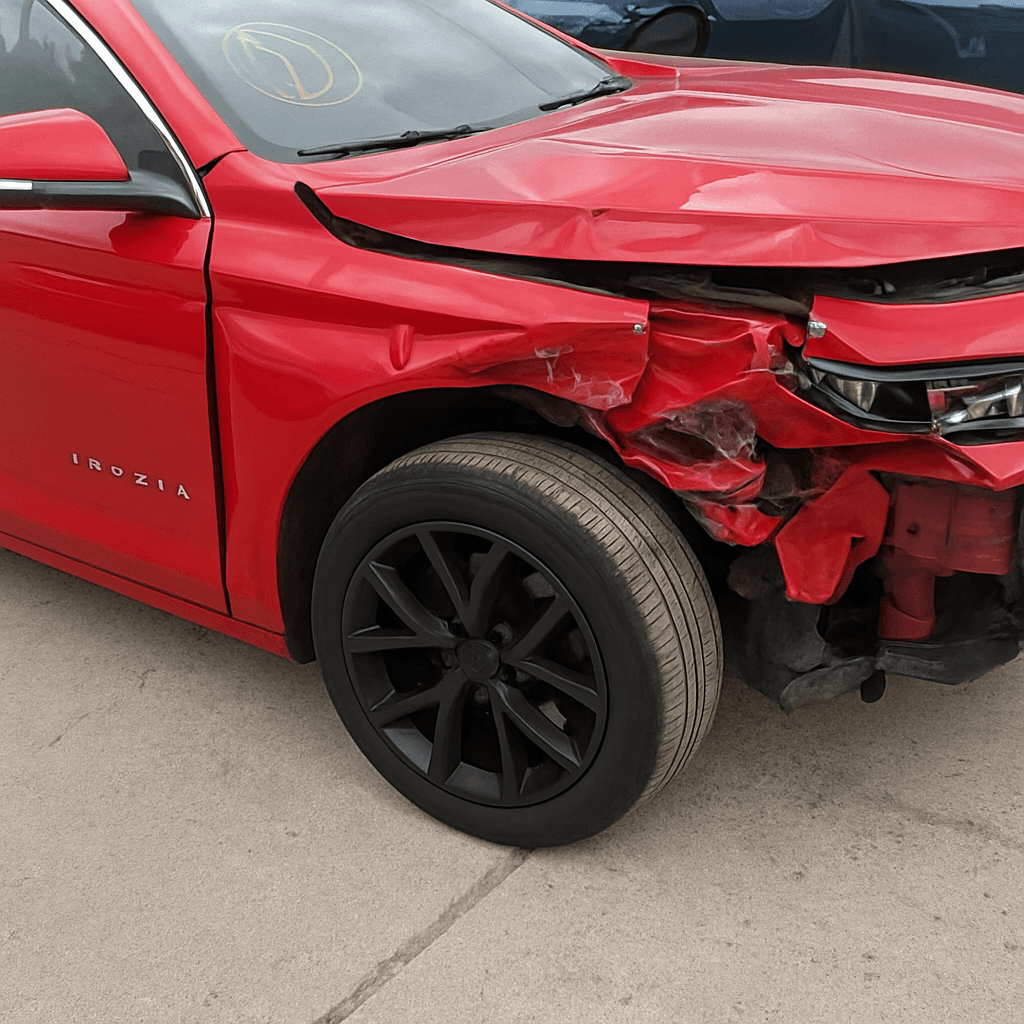

Collision pays when you hit another car, a guardrail, or roll the vehicle. Comprehensive pays when something other than a collision damages the car: theft, vandalism, hail, hitting a deer, flood. Both coverages pay the actual cash value of the vehicle at the time of loss, minus your deductible. If your 2016 sedan is worth $8,000 and you total it, collision pays $8,000 minus your deductible—you replace the car out of that check, or you don't replace it at all.

The lender required both coverages because the loan amount exceeded what you could afford to lose. Now that the loan is gone, the question flips: does the car's current value exceed what you can afford to lose? If the answer is yes, you still need the coverage. If the answer is no, you're self-insuring.

The blocker isn't the premium—it's whether you can write a check for a replacement car the day after a total loss without touching retirement funds you can't replenish.

The Replacement-Cost Test for Edison Drivers

Check your car's actual cash value on Kelley Blue Book or NADA, using the private-party value, not trade-in. A 2016 Honda Accord with 85,000 miles in good condition might show $10,000 to $12,000. That range is what collision or comprehensive would pay if you totaled the car tomorrow, minus your deductible. If your deductible is $500, you'd receive $9,500 to $11,500. Can you replace a comparable car for that amount out of your checking or savings account without touching funds earmarked for medical expenses, property taxes, or other non-discretionary costs?

If the answer is yes—you have $12,000 sitting in liquid savings and losing the car wouldn't force you to choose between transportation and another obligation—dropping collision and comprehensive becomes a calculated risk you can afford. If the answer is no, the coverage is still earning its cost. The premium is the price of not writing that check.

Related Articles

New Jersey-Specific Quirks That Bend the Standard Advice

New Jersey requires personal injury protection regardless of fault, which means your own medical bills after an accident are covered under PIP even if you drop collision and comprehensive. Medicare coordinates with PIP as the primary payer for accident-related injuries, but PIP pays first up to your selected limit. Dropping collision doesn't eliminate injury coverage; it eliminates vehicle-damage coverage.

New Jersey also uses a choice no-fault system, meaning you elected either a limited or unlimited right to sue when you bought the policy. That election affects your liability exposure and premium but has no effect on whether collision or comprehensive pays for your own car. The tort option you selected years ago doesn't change the replacement-cost test.

Edison's density and Route 1 commute traffic historically pushed collision claims higher than the state average, but if you no longer commute and drive under 5,000 miles per year, your collision risk profile has dropped significantly. That mileage reduction doesn't make collision unnecessary—it changes the actuarial probability, which should lower your premium if your carrier offers a low-mileage or usage-based program. Geico, Progressive, and Nationwide all write in New Jersey and offer mileage-tracking programs that can reduce collision premiums for drivers who log fewer miles.

NJ Mature-Driver Course Discount Floor

≥5%

New Jersey requires insurers to offer at least a 5 percent discount for completing a state-approved defensive driving course. The discount applies to all coverages, including collision and comprehensive, which means completing the course lowers the cost of keeping full coverage if you decide to retain it.

N.J.A.C. 11:3-24.3

What Happens When You Drop Coverage and Then Need It

You cannot add collision or comprehensive back mid-term and then file a claim for damage that occurred after you dropped it. The coverage applies only to losses that occur while the policy is in force with those coverages active. If you drop collision in March and total the car in June, you cannot reinstate collision retroactively. The car is a total loss and you're writing the replacement check.

Some drivers assume they can drop coverage during low-risk months and add it back before winter or a long trip. Carriers allow mid-term changes, but the coverage applies only going forward from the endorsement date. If you time it wrong, you're uninsured during the gap. The safer path is to keep the coverage year-round or accept that you're self-insuring fully once you drop it.

How to Lower the Cost Without Dropping Coverage

Raising your deductible from $500 to $1,000 cuts collision and comprehensive premiums by 15 to 25 percent depending on the carrier. If you have the higher deductible amount in liquid savings and can cover it in a claim, the premium reduction compounds over time. A $200 annual savings pays for the higher deductible in five years, and after that you're ahead.

Completing a state-approved defensive driving course triggers the statutory discount of at least 5 percent on all coverages. New Jersey-approved courses are available online and in person; check the New Jersey Motor Vehicle Commission's approved provider list before enrolling. The discount applies for three years in most cases, after which you can complete the course again to renew it. That 5 percent applies to collision and comprehensive, liability, and PIP together.

If you drive under 7,500 miles per year, ask your carrier whether they offer a low-mileage discount or a usage-based program. Geico, Progressive, and Nationwide all write in New Jersey and track mileage through mobile apps or plug-in devices. Collision premiums drop when annual mileage drops, because fewer miles means fewer opportunities for an accident. The discount isn't automatic; you have to enroll and verify mileage.

Make the Coverage Decision Match Your Actual Position

Pull your car's actual cash value from Kelley Blue Book or NADA today, subtract your current deductible, and compare that net figure against your liquid savings. If the net payout would force you to choose between replacing the car and covering another obligation, the coverage is still necessary. If the net payout is less than what you keep in liquid reserves for unplanned expenses, you're in a position to self-insure. Compare your current collision and comprehensive premium against the statistical likelihood of a total loss, then decide whether the annual cost is worth avoiding the out-of-pocket risk. That comparison is yours to make—no carrier, agent, or generic guide can make it for you.