Updated July 2026

What Is Liability Insurance Insurance?

Liability insurance has two parts: bodily injury liability covers medical bills, lost wages, and pain-and-suffering claims when you injure someone in an accident you caused; property damage liability pays to repair or replace the other driver's vehicle and any other property you damage. Your own repair bills and medical costs are not covered — liability flows in one direction only, from your policy to the people you harm. In New Jersey, your own injuries are covered under Personal Injury Protection regardless of fault, so liability's bodily injury component activates only when you injure someone else seriously enough to exceed the PIP threshold or when you're sued for pain and suffering.

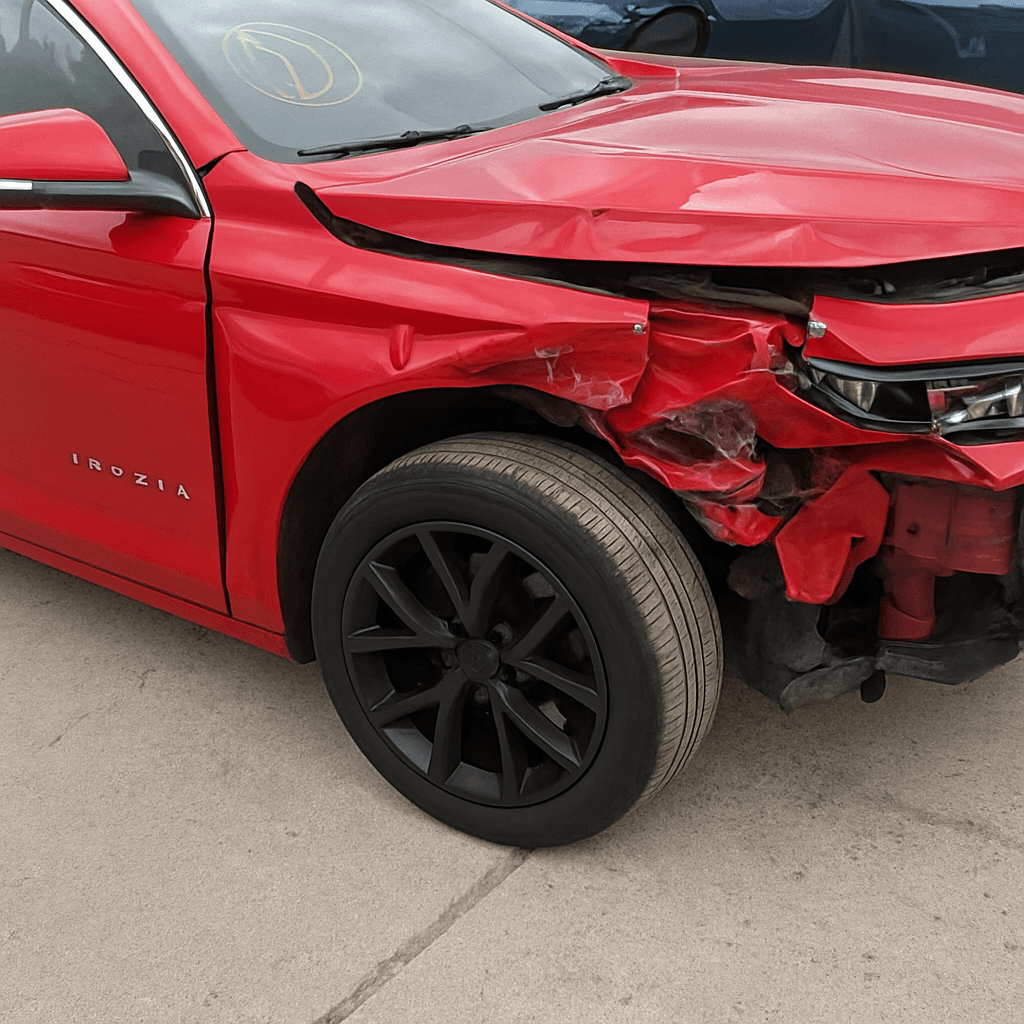

- You fail to stop at a red light and rear-end the car ahead. The other driver has $18,000 in medical bills and their vehicle sustains $9,500 in damage. Your bodily injury liability pays the $18,000 medical claim up to your policy limit. Your property damage liability pays the $9,500 repair bill. Your own vehicle damage is not covered by liability — you need collision coverage for that.

- You turn left on yellow and strike an oncoming motorcycle. The rider suffers $42,000 in medical expenses and files a pain-and-suffering lawsuit seeking $75,000. If you carry New Jersey's minimum $15,000 per person bodily injury limit, your insurer pays $15,000 and you are personally liable for the remaining $27,000 in medical costs plus the full lawsuit amount. Minimum limits do not cover severe injury claims — the gap comes from your assets.

- You back out of a grocery store space and scrape a parked SUV, causing $3,200 in paint and panel damage. Your property damage liability pays the claim in full. New Jersey requires only $5,000 in property damage coverage, but modern vehicle repair costs frequently exceed that floor — a single side-panel repair on a newer model often runs $4,000 to $6,000.

Who Needs Liability Insurance Insurance?

Retirees who still drive regularly and own assets worth protecting need liability limits well above New Jersey's $15,000/$30,000 minimum — a single severe injury claim can exceed that ceiling in minutes, leaving your retirement savings exposed to lawsuit. If you own a home, carry retirement accounts, or have meaningful savings, carry at least $100,000/$300,000 bodily injury and $100,000 property damage. Umbrella policies require underlying liability limits in this range, and the premium difference between minimum and adequate coverage is smaller than the financial devastation of a serious at-fault accident.

Calculate your net worth — home equity, retirement accounts, savings, and other assets a lawsuit could reach. Carry liability limits at least equal to that figure, or umbrella coverage above it. If you drive fewer than 7,500 miles per year, ask every carrier you compare about low-mileage and usage-based programs — the liability premium drops meaningfully when your exposure hours shrink. Minimum coverage saves $200–$400 annually but exposes you to six-figure personal liability in a single bad intersection decision.

How Much Does Liability Insurance Insurance Cost?

Liability-only policies in New Jersey typically add $40–$75 per month at state minimums; higher limits of $100,000/$300,000 bodily injury and $100,000 property damage add $65–$110 per month.

- Your at-fault accident history and violation record — a single at-fault claim in the past three years typically raises liability premiums 20–40 percent.

- The coverage limits you select — moving from minimum $15,000/$30,000 bodily injury to $100,000/$300,000 often doubles the bodily injury premium component.

- Your county and ZIP code — urban areas with higher claim frequency, such as Hudson and Essex counties, carry steeper liability rates than rural Burlington or Cape May.

- Annual mileage — retirees who drive under 7,500 miles per year qualify for low-mileage discounts with most New Jersey carriers, lowering liability cost 5–15 percent.

- Credit-based insurance score where permitted — New Jersey allows credit history to influence rates, and retirees with strong credit often see meaningfully lower liability premiums.

- Multi-policy and mature-driver discounts — bundling home and auto or completing an approved mature-driver course can reduce liability premiums 10–15 percent at many carriers.