Updated June 2026

What Is Collision Coverage Insurance?

Collision coverage repairs or replaces your vehicle after you hit another car, roll your vehicle, or strike a fixed object like a guardrail or pole. It pays regardless of who caused the accident. The insurer pays the repair bill up to your car's actual cash value minus your chosen deductible. If repair costs exceed the car's pre-accident market value, the insurer declares it a total loss and pays that value instead.

- You brake on a wet road and slide into a concrete barrier. Repair estimate: $4,200. Your car's actual cash value before the crash: $8,500. You carry a $500 deductible. Collision coverage pays $3,700. You pay the $500 deductible. Had you dropped collision to save the annual premium, you'd pay the full $4,200 out of pocket.

- You misjudge a lane change and sideswipe another vehicle. Your car's damage: $3,100. The other driver's damage: $2,800. Their medical bills: $6,400. Collision pays your $3,100 repair minus your deductible. Your liability coverage pays the other driver's $9,200 in vehicle and medical costs. Without collision, you'd cover your own $3,100 repair yourself.

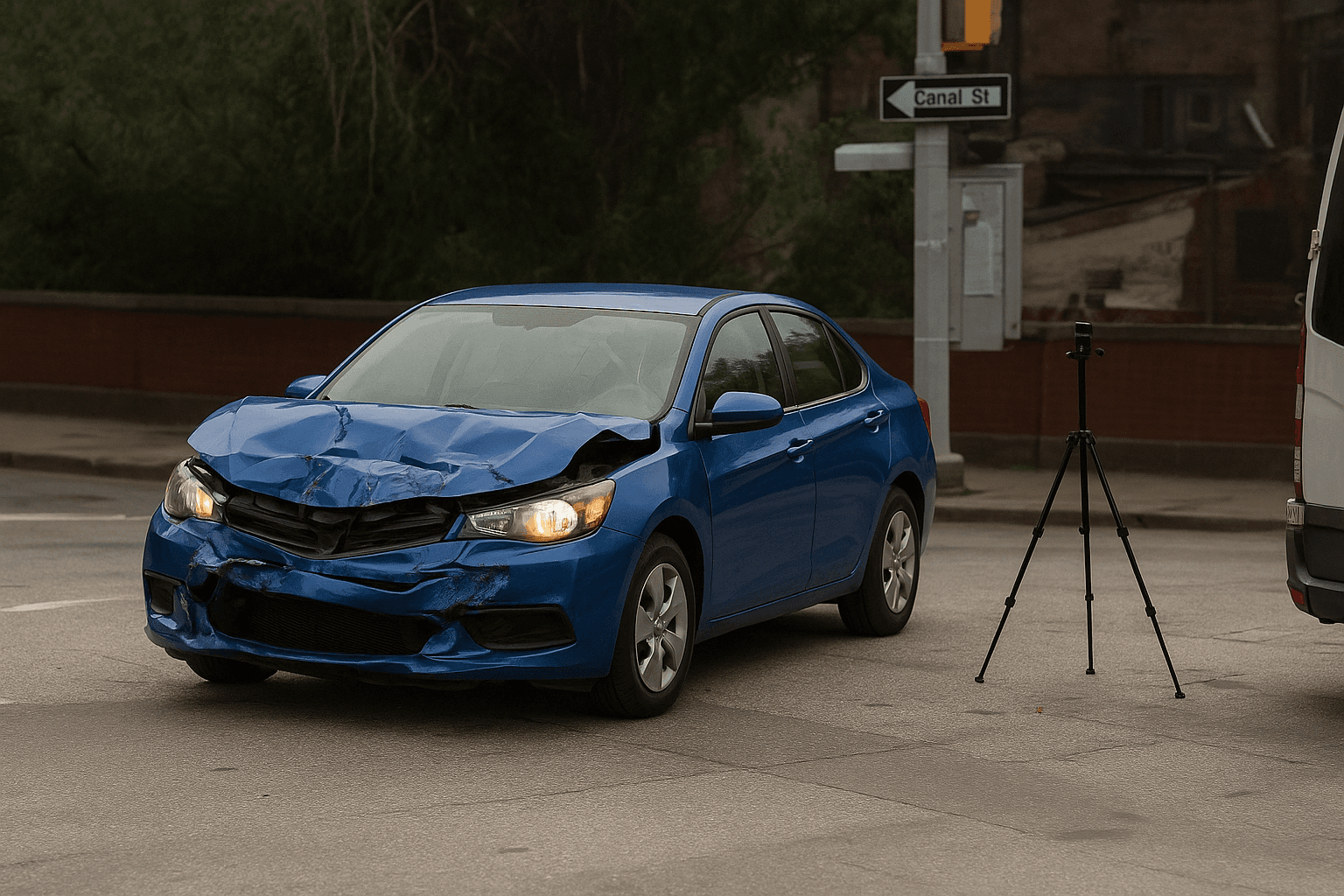

- You rear-end a stopped truck at 35 mph. Repair estimate: $11,000. Your car's actual cash value: $7,200. The insurer totals the vehicle and pays you $7,200 minus your $1,000 deductible: $6,200. You use that to buy a replacement. Had you carried no collision, the $11,000 loss falls entirely on you despite the car being worth only $7,200.

Who Needs Collision Coverage Insurance?

Carry collision if you're still financing your vehicle—the lender requires it. Also keep it if your car's current market value exceeds $5,000 and you lack liquid savings to replace it after a crash. Retirees who drive in dense traffic, park on streets in urban New Jersey counties, or have a history of minor fender-benders often find collision worth the annual cost.

Calculate break-even: divide your car's actual cash value by your annual collision premium plus deductible. If the result is under 3 years, you're likely overpaying. Check your state's low-mileage and usage-based programs—New Jersey carriers offer telematics discounts that can cut collision costs 15–30% for retirees driving under 7,500 miles per year, making retention more defensible.

How Much Does Collision Coverage Insurance Cost?

Collision typically adds $30–$90/month ($360–$1,080/year) to a New Jersey retiree's premium, depending on vehicle value, deductible choice, and driving record.

- Vehicle age and current market value—a 2015 sedan with $6,000 actual cash value costs far less to insure for collision than a 2022 model worth $28,000.

- Deductible selection—choosing a $1,000 deductible instead of $250 can cut collision premium by 25–40%, but you'll pay more out of pocket in any claim.

- Garaging zip code in New Jersey—urban counties like Hudson and Essex see higher collision rates and costlier repairs than rural Sussex or Warren, raising premiums 15–30%.

- Claims history—a single at-fault collision claim in the past three years can increase your collision premium by 20–50% at most carriers.

- Bundled discounts—retirees who pair auto and homeowners policies with the same carrier often see collision premiums drop 10–20%.